“Make a budget and stick to it” is one of the most common financial tips out there. Budgets are also one of the most misunderstood, misused, and misapplied tools in personal finance. If you’ve ever felt like budgeting should work but doesn’t (like you’re doing something wrong, or you just lack discipline) you’re not alone.

This article is about rethinking the budgeting conversation entirely. Instead of shaming ourselves into “sticking to a plan,” let’s take a closer look at the three most common types of budgeting, why they work (or don’t), and what actually helps reduce financial overwhelm.

Why Budgeting Often Fails

Most people don’t fail at budgeting because they’re bad with money. They “fail” because the system they’re using wasn’t designed for real life, especially a life that changes from month to month, includes more than one person, or involves emotional stress and competing values.

In coaching, we see it over and over: people try to implement a system they found online or got from a friend or podcast. It looks logical. Maybe it even works… for about two weeks. But as soon as life throws a curveball, an unexpected expense, a change in schedule, a stressful day, or even an unforeseen opportunity, the budget breaks.

And when it breaks, people don’t blame the budget. They blame themselves.

Let’s zoom out and look at the three most common budgeting philosophies, and how we can do better.

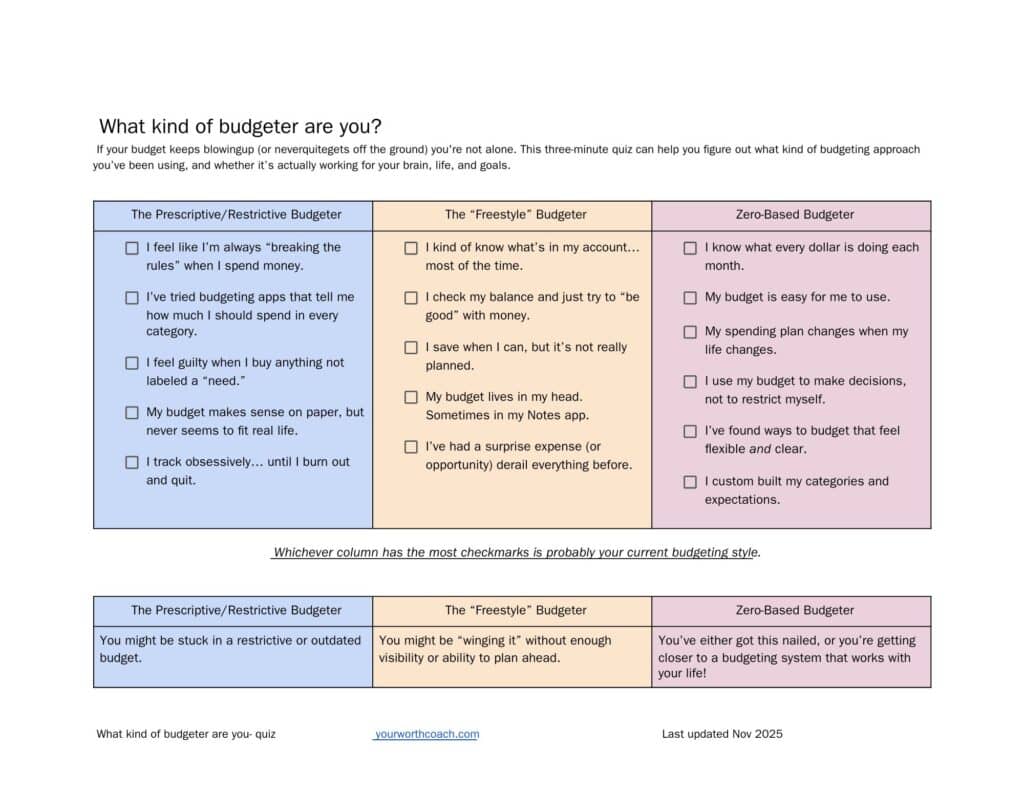

1. The “Percentage-Based” Budget

(aka: the traditional, restrictive, formula-based budget)

This is what most people picture when they hear the word budget. It’s prescriptive, cookie-cutter, and usually looks like a pie chart:

- 50% needs

- 30% wants

- 20% savings/debt

Or: - 15% to food

- 30% to housing

- 55% to “other spending”

The idea is that if you follow the right formula, you’ll be fine.

But here’s the problem: your life is not a formula.

Thought Experiment: The Teaching Scenario

Imagine you’re an incredible teacher. You’ve got 100 motivated, intelligent students, a world-class budgeting system designed by economists, and all the time you need to teach it well.

How many of those students will still be using the budget 30 days later?

In real life, the answer is: about 50. The rest quit by week two.

That’s not a people problem. That’s a system design problem.

Why this kind of budget fails:

- It expects life to be the same every month.

- It’s too rigid to flex with real circumstances.

- It doesn’t build in tools for adjustment, only discipline.

- Heavy focus on past-looking data with very little forward-thinking/planning.

These budgets sell the illusion of control and structure, but when they fail, we internalize that failure instead of questioning the method.

2. Freestyle Budgeting

(aka: “I kinda know what’s in my account… probably.”)

On the opposite end of the spectrum is freestyle budgeting, or rather, the absence of budgeting. This approach can mean people spend as needs and desires arise, maybe peeking at their bank balance now and then, but without a clear plan. BUT, it can also mean obsessively checking bank accounts, sometimes many times a day. Often the reason for this hyperfocus is to have a sense of some sort of control over finances, even if that means stress. Pressuring and stressing ourselves, however, is not the same as control and insight.

Going freestyle on your finances is not irresponsible. In fact, it often feels more flexible and kind. No rigid rules! Just vibes!

But freestyle budgeting has its own dark side.

Client Story: The Foreclosure That Wasn’t Their Fault

One of my earliest clients was a couple who had worked grueling overtime for months to save for a down payment. They gave up everything, family birthdays, eating out, travel, just to buy their first home. It was stunning how much work they did to get that down payment together. Then once they bought the home, they never made an on time payment, not once.

So, their home was foreclosed.

When we looked at the math, the reality was heartbreaking: there was no version of their budget where the mortgage made sense. But because they were stuck in freestyle, there was no way they could have known that.

Why freestyle budgeting fails:

- It creates financial blind spots.

- We often feel reactive, like we can’t see or plan into the future.

- It often leads to avoidant behaviors and stress loops and/or hyperfocus.

3. Zero-Based Budgeting (ZBB), Modified

(aka: the flexible, realistic approach you can actually sustain)

Zero-Based Budgeting isn’t new, but the way we use it in coaching is. Traditional ZBB gives every dollar a “job”. And leverages the expectation of intentional spending, not restriction.

We adapt it for real life: instead of micromanaging, we group expenses by purpose, build in flexibility, and assume life will change, so the budget should, too.

Analogy: “Big Car” Motor Company

Imagine a Big car’s 1985 budget, every dollar, department, and expense planned out. Now imagine handing that same budget, dollar-for-dollar, to the same company today.

Would it work?

Of course not. The company has changed. The world has changed. The budget must change too.

Now imagine you’re part of Big Car’s HR department. Midway through the year, the Sales department runs out of money and asks to borrow from you. Would you give them the money?

Nope, because in a well-run organization, every department has a purpose, and every dollar has a job. And, well, it’s not HR’s job to babysit the Sales department.

Ok, so now let’s say you (HR) have been given 10 million dollars to do your job for this two year biennium. But instead of spending that 10 million dollars, you’re going to restrict, and only spend one. BUT, you haven’t found a magical new way to do the job of HR on a 10th of the resources. Do you think you’d keep your job?

Not likely. Restriction doesn’t work within intentional spending plans like a ZBB. In fact, restriction can destroy an otherwise well-thought out, careful budget.

That’s how your household budget should work.

Why this works better:

- Flexibility is built-in, not bolted on.

- The budget is expected to evolve with you.

- It treats financial management like a system, not a shame cycle.

- You can see and plan into the future, instead of just reacting to the past.

So What Should You Do Instead?

Here’s what I recommend, whether you’re feeling overwhelmed, skeptical, or just tired of feeling behind:

Step 1: Track before you plan.

You can’t fix what you don’t understand. Start by tracking your spending without trying to correct or change your spending. Just observe!

Step 2: Sort by purpose.

Don’t just list “groceries” or “bills.” Ask: what is this for? Is it fuel, fun, care, connection? After all, Big Car company doesn’t sort by whether something is paid every week, only what is the purpose. Name your categories/departments based on the purpose of that spending TO YOU.

Step 3: Design a system, not a sentence.

Your budget isn’t a punishment. Build a structure that feels supportive and adaptable. Evaluate the system or routine, not yourself. In coaching I often hear “the budget is fine, I just have to stick with it.” If you can’t stick with it, the budget isn’t fine. Want another reframe? Find all the ways to budget that DON’T work for you.

Step 4: Talk it through.

For couples, 80% agreement is enough. Use budgeting as a relationship and communication tool, not a test. Return to Step 2 if “we don’t really need that” or “we don’t buy this every month” start to creep in. Big Car company treats all spending as important in some way (otherwise they wouldn’t be spending on it). And Big Car company doesn’t sort by the frequency of the spending, only its purpose.

Step 5: Expect change.

Every budget is a draft. Every plan is a work in progress. That’s not a failure, that’s the point.

If Budgeting Has Never Worked for You… It’s Not You

You are not lazy. You are not broken. And you’re not “bad with money.”

You’ve just been handed the wrong tools.

It’s time to trade the shame spiral for a system that actually fits your life.

Want to try zero-based budgeting that actually works?

Book a free info session, and let’s rebuild your system together, no judgment, no restriction, no cookie-cutter templates.